House view: staying invested, being diversified

A resilient global cycle continues to support calculated risk taking. Global growth remains solid, inflation is easing and policy is gradually loosening — all supportive for asset markets, despite the risks.

24th February 2026 11:09

by Aberdeen Investments from Aberdeen

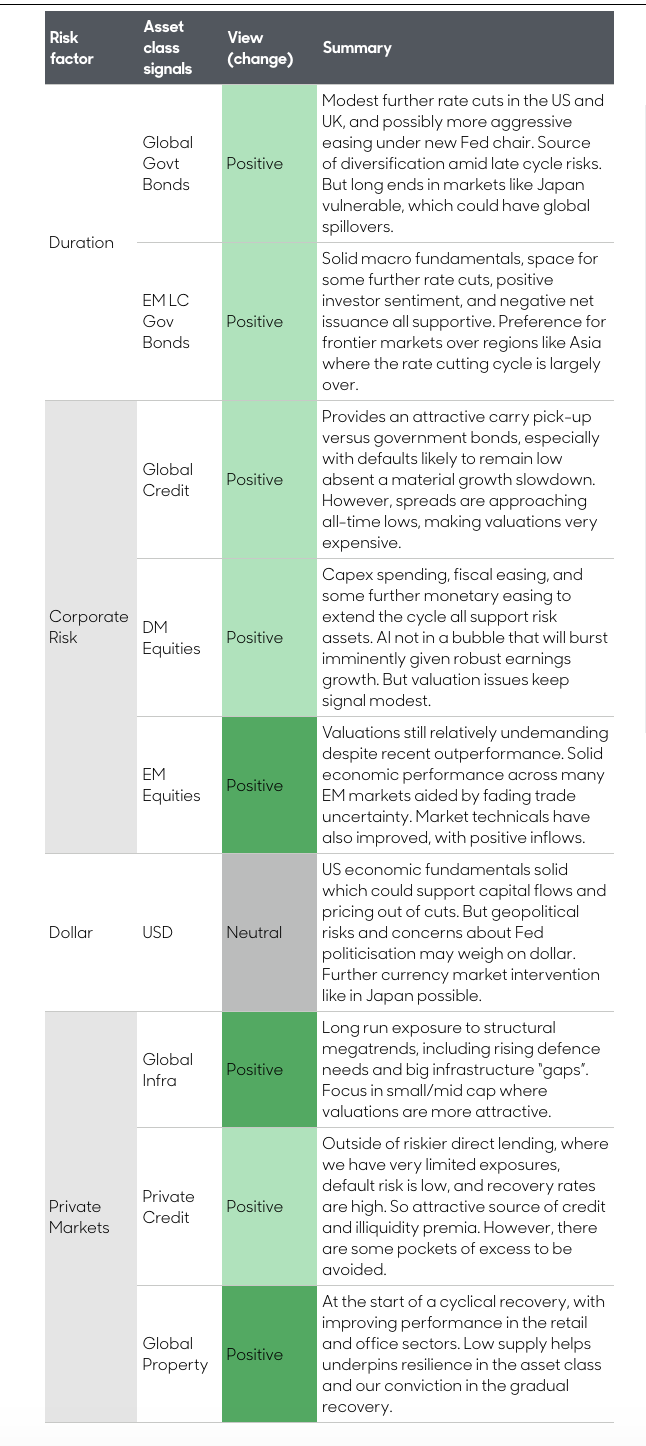

Our House View retains a pro-risk stance with the strongest convictions in emerging market equities, property and infrastructure. Bonds should help diversify cyclical risks, while a neutral dollar can underpin global carry trades.

We expect a year of slightly above-trend global growth (3.1%). US growth is likely to be strong at 2.5%, supported by AI-driven investment, positive stock market wealth effects, fiscal easing and reduced trade uncertainty. US inflation may temporarily push higher due to delayed tariff pass-through, but underlying price pressures remain contained and inflation should ease back toward target by year-end.

We are forecasting the US Federal Reserve to hold interest rates for the remainder of Chair Jerome Powell’s term and then deliver two 0.25-percentage point cuts later in the year. Incoming chair Kevin Warsh is a credible pick, removing some of the politicisation concerns around the central bank. However, he may look to shrink the Fed's footprint in the Treasury market.

Politics and geopolitics remain a source of considerable uncertainty globally. A structurally more volatile geopolitical environment will keep inflation volatility elevated and reduce the diversification coming from bonds, meaning investors need to find alternative sources of diversification. It also raises questions about allocations to dollar-based assets because the US is the source of much of this uncertainty.

However, the baseline of positive global growth is supported by fiscal loosening in the likes of the US, Europe and Japan. Moderating inflation and ongoing monetary easing in many economies should provide a constructive backdrop for risk assets.

Corporate risk: positive bias, especially toward EM

Corporate earnings remain strong, particularly in technology and financials. Despite recent wobbles, AI-related equities are not (yet) in bubble territory: earnings growth remains robust, leverage is low among major tech firms and real-world use cases continue to broaden.

That said, with the level of investment within this sector, an AI correction is one of the key risks we are watching. With valuations full for US equities, we prefer non-US markets.

Indeed, emerging market (EM) equities remain attractive, with valuations still undemanding, resilient earnings (notably in semiconductors), and improving market technicals as investment inflows return. China’s economic slowdown looks manageable, supported by policy easing and improved investor sentiment linked to AI-related themes.

Global bonds: protection against downside demand shocks

We maintain a positive view on government bonds. The possibility of the US labour market cracking and the likelihood of renewed easing under the next Fed chair, should support this asset class. That said, yields for bonds with longer maturities may remain elevated given fiscal pressures and higher term premia, but shorter duration debt should perform well in a cutting cycle.

Meanwhile, EM local-currency debt remains supported by improved macro fundamentals, reduced net issuance and still-favourable carry, even though more of the rate cutting cycle lies behind us than ahead.

Dollar: neutral on conflicting drivers

We expect the dollar to remain range-bound. The strong US growth outlook should be supportive of the dollar. And one source of potential dollar downside — a politicised Federal Reserve — seems to have abated with the appointment of Kevin Warsh.

But the US remains the primary source of political and geopolitical risk in the global economy, so we expect capital to continue to flow out of US assets towards more attractively valued EM and European markets. On balance, the signal is neutral the dollar, and this should support global carry trades.

Private markets: constructive across private credit, property and infrastructure

Private credit. Upgraded to modestly positive. We see opportunities in high-quality, investment-grade lending that come with low default rates and high recoveries. That said, there is more credit risk in direct lending.

Real estate. Upgraded to positive. The cyclical recovery has begun, supported by improving fundamentals, constrained new supply and supportive rate dynamics. Our preferred sectors include apartments, offices and industrials.

Infrastructure. Remains positive. Structural themes — including digitalisation, decarbonisation and the need for private capital to supplement stretched government balance sheets — continue to provide long-term support.

Key risks

Major risks include: a flare-up in geopolitical tensions causing oil prices to spike and broad risk-off sentiment to dominate; a potential AI-driven equity correction spilling into the real economy; renewed US tariff shocks; US labour-market weakness evolving into a broader downturn; and threats to Fed independence undermining US institutional credibility.

However, there are also upside risks from a strong AI-driven productivity improvement. Our investment approach emphasises scenario analysis and stress-testing to understand exposure to these risks and diversification to mitigate potential drawdowns.

Overall positioning

Our House View maintains a pro-risk stance, with the strongest convictions in EM equities, infrastructure and global property. Bonds can play a diversification role against some of the cyclical risks, while our neutral-dollar view supports global carry opportunities. All told, the macro environment — resilient growth, easing inflation and incremental policy loosening — remains supportive of calculated risk taking in portfolios.

For more details on the latest House View see below:

Table 1: Aberdeen House View: February 2026

Source: Aberdeen, February 2026. The views expressed should not be construed as advice or an investment recommendation on how to construct a portfolio or whether to buy, retain or sell a particular investment. Forecast is offered as opinion and is not reflective of potential performance. Forecast is not guaranteed and actual events or results may differ materially.

ii is an Aberdeen business.

Aberdeen is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.