Shares for the future: 2026 a low point for very profitable firm?

This stock ranks in analyst Richard Beddard’s top 10 and is fighting with last week’s share for the future for a place in his Share Sleuth portfolio.

19th June 2026 15:00

by Richard Beddard from interactive investor

This month’s Share Sleuth trade is shaping up as a head-to-head between adding Keystone Law Group Ordinary Shares (LSE:KEYS), which I evaluated last week, and Judges Scientific (LSE:JDG), this week’s subject. The portfolio does not own shares in either.

- Invest with ii: Share Dealing with ii | Open a Stocks & Shares ISA | Our Investment Accounts

Difficult patch

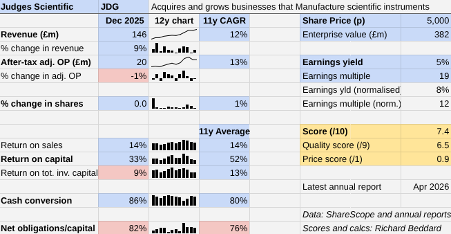

Although the year to December 2025 was a sub-par year for Judges Scientific, it was better than 2024 and 2026 probably will be.

Revenue grew 9% versus a 2% decline in 2024. Adjusted profit declined 1%, compared to a 21% decline. The net debt to capital ratio was high (boo) but typical. Cash conversion was also high (hooray) and also typical.

Judges’ long-term financial performance is still impressive, with double-digit revenue and profit growth and high Return on Capital employed. But it is an exporter of financial instruments adjusting to a world in which there is more trade friction and lower funding for higher education.

Revenue in 2025 was flattered by a so-called coring expedition. These add an element of unpredictability to Judges’ performance because they don’t happen every year.

Judges’ biggest ever acquisition, Geotek, mounts these expeditions. Acquired in 2022, it is unusual among Judges’ many acquisitions. In addition to manufacturing scientific equipment, it provides services.

Chief among these is collecting and analysing geological cores. These are large-scale technical projects hitherto sponsored by governments. They support oil and gas field development, siting wind turbines, tunnel and pipeline design, mineral exploration and research.

- DIY Investor Diary: how I mix tech and dividends

- How to build a World Cup-winning portfolio

- How the experts would invest a SIPP at every life stage

Geotek has achieved its expectation of three expeditions every four years in its first four years under Judges. It missed 2024, though, and the company doesn’t expect one in 2026. This clouds the outlook, which was already threatening because of a decline in orders.

I estimate coring added just over 4% to revenue in 2025. In 2023, it added about 5.5% to revenue. Coring is very profitable though, and without it the company anticipated a decline in earnings per share of between 9% and 20% in the year to December 2026, when it published full-year results in March.

Judges will update us when it publishes half-year results, probably at the end of July.

Roll-up strategy

Since 2005, Judges’ strategy has been to roll-up founder-led scientific instrument manufacturers. It acquires highly profitable businesses in narrow niches.

In theory and generally in practice, these companies slough off more cash than they need to grow. Judges uses the excess cash to pay off the debt used to acquire them.

The profitability of this strategy is dependent on the availability of finance to pay for the acquisitions and founders wishing to move on and sell businesses.

Higher interest rates may put this strategy under pressure, because the requirement to service interest payments will, other things being equal, mean less cash to pay down the debt.

Other things are not always equal. When the cost of acquisitions goes up, founders might place lower values on their businesses to encourage reluctant buyers, reducing the amount of debt required.

It is difficult to judge how this is playing out from Judges’ acquisition history, because Geotek was Judges’ biggest acquisition by far, and subsequent acquisitions have been modest.

That may be because Judges cannot find targets that meet its strict criteria, or it may be that, having leveraged up to buy Geotek, the company lacks the capacity for a big acquisition.

- New state pension proposal highlights challenges for younger workers

- How retirees can manage inflation and interest rate uncertainty

Geotek demonstrates another factor that may reduce Judges’ pace of growth. Larger targets attract more suitors because there are fewer of them, and they are more likely to make a difference to well-resourced private equity firms and listed rivals.

Judges’ policy is not to pay more than 7 times EBIT (profit before interest and tax), a limit it hit with Geoteck. Now that it is big enough to play in this field, it will probably have to pay top whack more often.

The success of the strategy also depends on the quality of the businesses Judges acquires. 2025’s results were, to my mind, a bit humbling.

Although Judges reversed the previous year’s impairment in the value of GeoTek, it wrote off all the goodwill relating to Armfield, acquired in 2015, citing “a prolonged period of underperformance”.

Judges also wrote down the value of Rockwash, a company that it had acquired less than a year earlier, due to its “reduced short-term outlook”. While this means Judges won’t pay as much for the company, because much of the cost was in the form of an earnout based on Rockwash’s performance, we wait to see if its troubles persist.

At 9%, and for the second year running, Return on Total Invested Capital (ROTIC), a measure of profitability that incorporates the full (unamortised) cost of acquisitions, dipped below 10%.

This level of return brings into question the prices Judges has paid for acquisitions in aggregate.

International growth

To grow their small niches Judges’ subsidiaries must be able to penetrate export markets. Local markets are rarely big enough. This aspect of Judges’ business model also appears to be less reliable in the 2020s than it did previously.

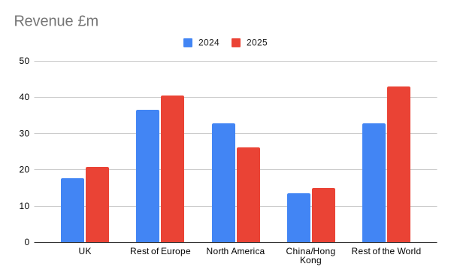

Protectionism in the US, Judges’ biggest single country market, and lower funding for higher education has reduced the attraction of the North American market.

Globally, more than half of Judges’ customers are educational institutions, and revenue fell 20% in North America in 2025. Judges believes funding will return because a five-year spending package was approved by Congress earlier this year, but it is uncertain about the extent and timing.

- Ian Cowie: how I’m investing in space

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Trade sanctions, and heightened Chinese competition has reduced Judges’ expectations of growth there too, to roughly the group’s aggregate growth rate. In 2025, it exceeded that marginally, when Chinese revenue grew 11%.

Judges is not slavishly dependent on these markets. It earns most of the revenue outside them. But in the UK and Europe, many teaching and research institutions are competing for scarce government funds.

Responding to these headwinds, Judges is doing what it can: fostering a growth mindset in its subsidiaries and sharing know-how to boost organic growth.

At Fire Testing Technology (FTT), for example, it is in the middle of a multi-year refresh of its ageing product line to better withstand competition. FTT was Judges’ first acquisition in 2005. It supplies instruments for testing materials to fire standards.

Scoring Judges Scientific

Risks abound but the combination of disciplined acquisition and innovation has driven growth at much bigger businesses, like Halma (LSE:HLMA), from which Judges has recruited.

Although employee turnover is quite high (19% in 2025), Judges has a reputation for being an “honourable acquirer” by sticking to the terms of deals as they progress.

Founder and former chief executive David Cicurel instituted this culture. He resigned earlier this year, making way for Tim Prestidge, previously business development director.

Cicurel chairs an experienced board and is still involved in acquisitions alongside Rik Armitage, who joined as acquisitions executive (a non-board position) during the year.

| Judges Scientific | JDG | Acquires and grows businesses that manufacture scientific instruments | 17/06/2026 | 7.4/10 |

| How capably has Judges Scientific made money? | 3.0 | |||

| Under consistent management, Judges Scientific has achieved double-digit revenue and profit CAGRs, high levels of profitability and strong cash flows by buying and operating niche manufacturers of scientific instruments. | ||||

| How big are the risks? | 1.0 | |||

| As Judges Scientific grows, it is buying pricier and more complex businesses. At 86% of operating capital, financial obligations are high by my standards but typical of Judges’. Protectionism in the US and China, and funding pressure on higher education means growth may be harder to come by. | ||||

| How fair and coherent is its strategy? | 2.5 | |||

| Scientific instruments enable research, which is beneficial to humanity. The company’s strategy is to roll up more businesses. It is also doing more to foster organic growth, perhaps mitigating challenging growth prospects somewhat. | ||||

| How low (high) is the share price compared to normalised profit? | 0.9 | |||

| Low. A share price of 5,000p values the enterprise at £382 million, about 12 times normalised profit. | ||||

| NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explained here) | ||||

With coring revenue anticipated in 2027, and perhaps a rebound in higher education spending, 2026 may be a low point for a still very profitable firm.

Over the next decade, though, I wonder if a bigger Judges in a less stable world will find it harder to achieve the double-digit growth rates that it has in the last decade.

A score of 7.4 ranks Judges Scientific 10th in the Decision Engine table below, one position behind Keystone Law (score 7.5)!

30 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score more than 5 out of 10 to be worthy of long-term investment in sizes determined by the ideal holding size (ihs%).

Anpario (LSE:ANP), Autotrader Group (LSE:AUTO), and Oxford Instruments (LSE:OXIG) have published annual reports and are due to be re-scored.

| company | description | score | qual | price | ih% | |

| 1 | FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.9 | 9.0 | 0.9 | 9.9% |

| 2 | James Latham | Distributes imported panel products, timber, and laminates | 8.5 | 7.5 | 1.0 | 7.0% |

| 3 | Hollywood Bowl | Operates tenpin bowling centres | 8.3 | 8.0 | 0.3 | 6.6% |

| 4 | Renew | Maintains and improves road, rail, water, and energy infrastructure | 8.2 | 7.5 | 0.7 | 6.4% |

| 5 | Jet2 | Flies people to holiday locations, often on package tours | 8.0 | 7.0 | 1.0 | 6.0% |

| 6 | Porvair | Manufactures filters and laboratory equipment | 8.0 | 8.0 | 0.0 | 5.9% |

| 7 | Solid State | Manufactures electronic systems and distributes components | 7.8 | 7.0 | 0.8 | 5.7% |

| 8 | Howden Joinery | Supplies kitchens and joinery to builders and online to DIYers | 7.8 | 7.0 | 0.8 | 5.5% |

| 9 | Keystone Law | Operates a network of self-employed lawyers | 7.5 | 7.0 | 0.5 | 4.9% |

| 10 | Judges Scientific | Acquires and grows businesses that Manufacture scientific instruments | 7.4 | 6.5 | 0.9 | 4.8% |

| 11 | Bunzl | Distributes essential everyday items consumed by businesses | 7.4 | 7.0 | 0.4 | 4.8% |

| 12 | Auto Trader | Online marketplace for motor vehicles | 7.4 | 6.5 | 0.9 | 4.8% |

| 13 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 7.2 | 6.5 | 0.7 | 4.3% |

| 14 | Cake Box | Cake shop franchise and sweet manufacturer | 7.1 | 7.0 | 0.1 | 4.2% |

| 15 | Volution | Manufacturer of ventilation products | 7.1 | 8.5 | -1.4 | 4.2% |

| 16 | Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 7.1 | 6.5 | 0.6 | 4.2% |

| 17 | Churchill China | Manufactures tableware for restaurants etc. | 7.0 | 6.0 | 1.0 | 4.0% |

| 18 | Focusrite | Designs recording equipment, synthesisers and sound systems | 7.0 | 6.0 | 1.0 | 4.0% |

| 19 | YouGov | Surveys public opinion and conducts market research online | 6.9 | 6.0 | 0.9 | 3.9% |

| 20 | Anpario | Manufactures natural animal feed additives | 6.8 | 7.0 | -0.2 | 3.5% |

| 21 | Games Workshop | Designs, makes and distributes Warhammer. Licenses IP | 6.7 | 8.5 | -1.8 | 3.5% |

| 22 | Quartix | Supplies vehicle tracking systems to small fleets | 6.7 | 7.0 | -0.3 | 3.4% |

| 23 | Goodwin | Casts and machines steel and processes minerals for niche markets | 6.6 | 7.5 | -0.9 | 3.3% |

| 24 | Softcat | Sells software and hardware to businesses and public sector | 6.6 | 7.0 | -0.4 | 3.3% |

| 25 | Cohort | Manufactures/supplies defence tech, training, consultancy | 6.6 | 8.0 | -1.4 | 3.2% |

| 26 | Macfarlane | Distributes and manufactures protective packaging | 6.5 | 5.5 | 1.0 | 3.0% |

| 27 | Bloomsbury Publishing | Publishes books and educational resources | 6.3 | 7.5 | -1.2 | 2.5% |

| 28 | Tristel | Manufactures hospital disinfectant | 6.0 | 8.0 | -2.0 | 2.5% |

| 29 | 4Imprint | Customises and distributes promotional goods | 5.8 | 8.0 | -2.2 | 2.5% |

| 30 | Renishaw | Makes tools and systems for manufacturers | 4.5 | 6.5 | -2.0 | 2.5% |

Click on a share's score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, and ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.