The trusts tipped to unlock untapped upside

China is the next country to see the potential benefit of executing corporate governance reforms, says one Kepler analyst who examines the trusts positioned to capture it.

13th February 2026 14:02

This content is provided by Kepler Trust Intelligence, an investment trust focused website for private and professional investors. Kepler Trust Intelligence is a third-party supplier and not part of interactive investor. It is provided for information only and does not constitute a personal recommendation.

Material produced by Kepler Trust Intelligence should be considered a marketing communication, and is not independent research.

After its origins in the Ganges plains in northern India, Buddhism grew gently over the centuries, spreading into China via the Silk Road, before taking hold in Korea and later Japan in the 6th century. The religion’s teachings and ideals were soon adopted into each country’s government and belief systems, becoming central to how their states operate and how their cultures have evolved.

Over the past few years, this journey has been taken in reverse through an unlikely source: the adoption of corporate governance reforms. Having begun in Japan over a decade ago, the concept of new rules and regulations for the betterment of minority shareholders has since been adopted by South Korea, and more recently, China.

This has begun to have positive effects, most notably through improved dividend payouts and some limited rallies in specific stocks. However, much like the centuries-long growth of Buddhism, these measures have not had an immediate, widespread impact, and as such, we believe there is untapped upside on offer, with several investment trusts well placed to capture it.

Shinzo starts off

The model for large-scale corporate governance reforms began in Japan over a decade ago by the prime minister at the time, Shinzo Abe, as part of his ‘Three Arrows’ policy to economic prosperity. This top-down set of structural reforms brought in improved measures for companies designed to tackle some of the institutional problems that existed, with the ultimate aim of making the market more attractive for global investors.

This included codifying rules on corporate governance, such as appointing independent directors; the introduction of improvements to stewardship, through a pickup in shareholder engagement; and, crucially, reforms on the use of capital, through reducing the level of excess cash companies had been holding on to, and putting this towards higher dividends and share buybacks.

While these measures were announced back in 2012, they didn’t have an immediate effect, with corporate culture taking a while to adjust. However, the pace of adoption has increased recently, aided by several revisions to the codes, as well as a pressure campaign by the Tokyo Stock Exchange, which includes naming and shaming those with a price-to-book (PB) ratio below 1.0x and a return on equity under 8%.

Eventually, these have begun to show results in the TOPIX, a market comprised of all the companies listed on the First Section of the Tokyo Stock Exchange. First, governance has improved, with the number of boards comprising over a third of independent directors increasing from 12% in 2015 to 95% in 2023, with those having separate nomination and remuneration committees rising from 11% and 13% respectively, to 88% and 89% over the same time periods. There have been other benefits, too, such as zombie companies being delisted and stricter liquidity requirements, something we discussed in another article.

This has also improved investor returns. Aggregate payout ratios for the index have increased notably since 2020 and have begun to close the gap on developed market counterparts. Market valuations are picking up too, with the TOPIX aggregate PB ratio up to 1.8x, almost 50% above its ten-year average of 1.3x. Meanwhile, the market itself has climbed to record highs, with a total return since the beginning of 2015 of over 150%.

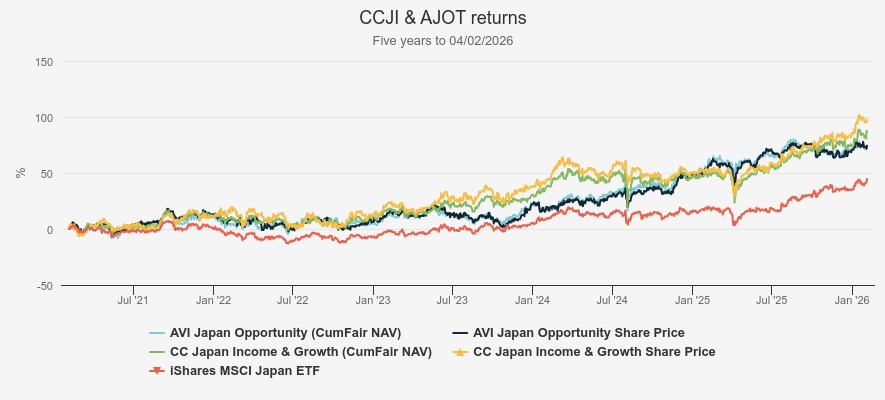

While this has been impressive, the managers of CC Japan Income & Growth Ord (LSE:CCJI) note there is plenty more work to do. They highlight that 58% of listed companies still have net cash, versus equivalent figures of 31% for the UK’s FTSE All-Share, 20% for the US’ S&P 1500, and 14% for MSCI Europe.

In fact, the figure for Japan has actually increased very slightly, from 57% in 2016. CCJI was launched in 2015, specifically designed to capture the upside in Japanese companies as a result of the wave of corporate governance reforms. This has served returns well, with CCJI returning 234% NAV total return since launch to 04 February 2026, considerably ahead of the TOPIX, which returned 163.5% over the same period.

AVI Japan Opportunity Ord (LSE:AJOT)is another trust that launched specifically to capture the opportunities thrown up by the revolution in corporate governance. Manager Joe Bauernfreund takes a more activist approach, engaging with companies to encourage them to boost their financial performance and make their balance sheets more efficient, aiming to generate strong returns when these are enacted. Returns have again been very strong, with AJOT delivering a total NAV return of 96.3% since inception on 23 October 2018, considerably ahead of the TOPIX, which delivered 78.7%.

We have shown the five-year performance of both trusts in the chart below, using an ETF as a proxy for the TOPIX.

Five-year Japan returns

Source: Morningstar. Past performance is not a reliable indicator of future results

How to solve a problem like Korea

Following success in Japan, these reforms have become the blueprint for others to follow. Korea has arguably done exactly that with the announcement of its ‘Value up’ programme in 2024, something we discussed in a previous note. This was done to improve the treatment of minority shareholders, as well as reduce the influence of the complex chaebol system in the country, which describes the series of large family-run conglomerates with cross-company shareholdings which exert control over a web of listed companies.

As for their neighbours across the Tsushima Strait, Korea’s Value up programme started slowly, before finding success with the banks and car makers, which then spread to other industries, having a profound effect on markets. In fact, Korea was the best-performing major Asian market in 2025, with the Value up programme cited as a significant influence.

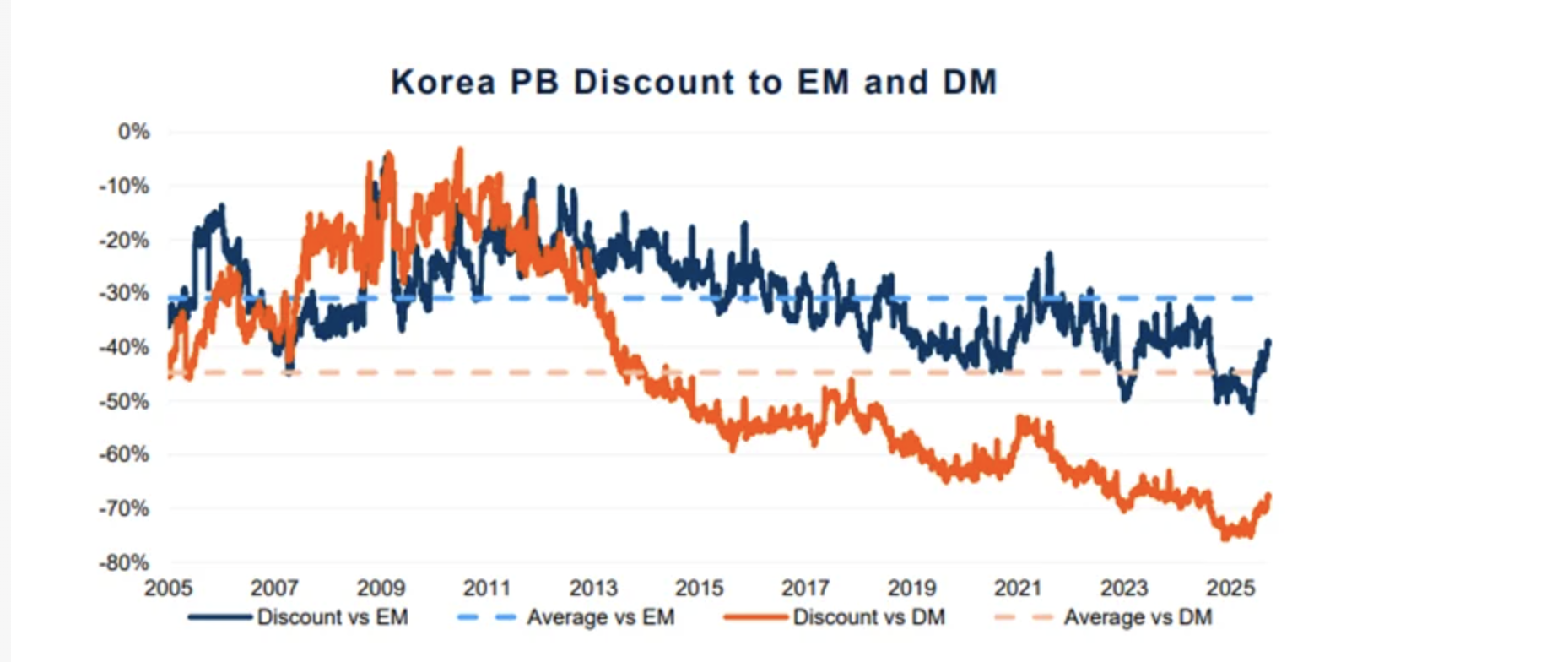

Having successfully capitalised on the reform opportunity in Japan, Joe Bauernfreund, who also manages the AVI Global Trust Ord (LSE:AGT), has identified similar potential in Korea. He notes that their reforms have several years to run, with the ultimate goal of Korea reaching developed market status. As such, there is considerable incentive for the recently elected government to keep pushing these, having seen the success they have had so far. In terms of opportunity, he notes that despite the recent recovery, the Korean market still trades at a notable discount to the emerging market index and an even bigger discount to developed markets, which they aim to become, meaning this gap could continue to narrow over the next few years, with the potential for strong returns.

Korean discount

Source: AVI, as at 30/09/2025.

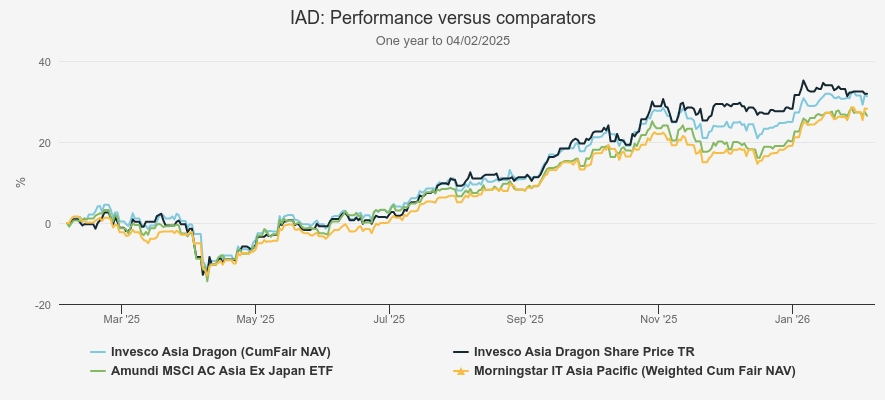

Fiona Yang and Ian Hargreaves, managers of Invesco Asia Dragon Trust Ord (LSE:IAD), have also identified a number of opportunities in Korea in recent years. They note the significant increase in dividends, which have gone from an average of c. 20KRW per share in 2005 to c. 70KRW in 2025, as well as the higher share buybacks as some of the key factors behind this. Korea was a notable driver of the trust’s strong performance in the past year, which rose 31.3% to 04 February 2026, versus the MSCI Asia ex Japan Index, which was up 30.1%, with Fiona and Ian noting that Value up was a considerable catalyst. As a result of their contrarian, value-focussed mindset, the managers have begun taking profits in their Korean holdings, with the country around neutral weight at the turn of the year.

IAD one-year performance

Source: Morningstar. Past performance is not a reliable indicator of future results

All the G in China

The Korean story is starting to get out there, but we think there is a much earlier stage story developing in China, which could be really exciting. Following in the footsteps of its Asian peers, the Chinese government, and regulators have announced a series of corporate governance reforms designed to increase the competitiveness of their market.

This process began at the end of 2023, with significant revisions made to company law, which came into effect in mid-2024 and was quite high-level, providing better rights for shareholders and clarity on board structures. This was built upon with the ‘national nine articles’ in 2024, which further enhanced corporate governance and investor protection rules. Throughout the rest of 2024 and into 2025, there were a series of new initiatives launched, with changes to investor relations rules, updates to director duties, implementations of international norms such as audit committees for listed firms and, most pertinent, to many investment trusts focussed on the country, an active push for an increase in dividends and share buybacks. The aim of the latter was to increase long-term capital allocations from the likes of institutional investors and pension funds.

However, whilst these reforms have been wide ranging with the potential to have a similarly transformative approach, they haven’t received the same level of attention that Japan and Korea have. There are arguably several reasons behind this. For one, they have come out piecemeal, in a series of announcements over a prolonged period, meaning each one hasn’t had much of an effect. However, when combined, they have a lot of potential upside. Similarly, these initiatives have been named individually, rather than under an all-encompassing programme such as ‘Value up’, which gives investors something to direct their focus on. Instead, these reforms have somewhat technocratic titles such as “Opinions on Strengthening Supervision, Preventing Risks and Promoting the High-Quality Development of the Capital Market”, making them difficult to decipher and not enticing to read. Finally, there is the context of the Chinese investment environment during their announcement period, which has taken much of the attention.

Over the period these reforms were announced, China has gone from seriously out of favour to one of the best-performing markets in the region. Back in 2024, the country had been struggling with a housing crisis and a collapse in consumer confidence, but after a series of government stimulus measures in 2024, the country went on a significant rally, which we have discussed in a previous article. As a result, much of the discussion of China’s investment case has instead focussed on the potential of stimulus measures, rather than reform, and as such, we think the potential impact of these reforms has been overlooked.

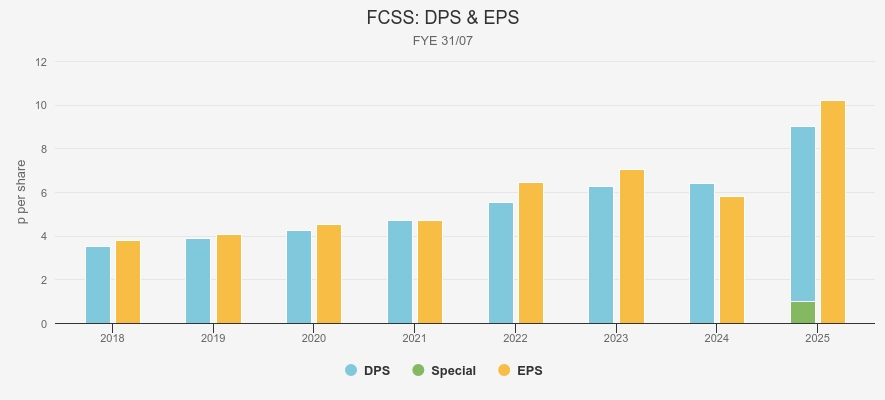

The recent dividend increase of Fidelity China Special Situations Ord (LSE:FCSS) is one example of these policies having a notable impact. In 2025, the trust increased its ordinary dividend by 25% on the previous year, aided by record high revenue generation of almost double the year prior. As a result, the trust was also able to pay its first-ever special dividend and increase revenue reserves for future years, with the trust’s current yield on the ordinary shares of 2.6%.

FCSS dividend & earnings growth

Source: Fidelity.

Furthermore, a big increase in portfolio companies buying back their shares has boosted the trust’s NAV. In the year to 31/08/2025, the second biggest contributor to relative performance was financials firm LexinFintech, which performed well after the announcement of a share buyback programme in July 2025, which equates to between 5% and 10% of market cap. This is a pattern repeated elsewhere in the Chinese market, with Fiona Yang and Ian Hargreaves of IAD also noting high share buybacks from the likes of NetEase Inc ADR (NASDAQ:NTES), JD.com Inc ADR (NASDAQ:JD), and H World Group Ltd ADR (NASDAQ:HTHT), of which the latter two saw significant share price rises as a result.

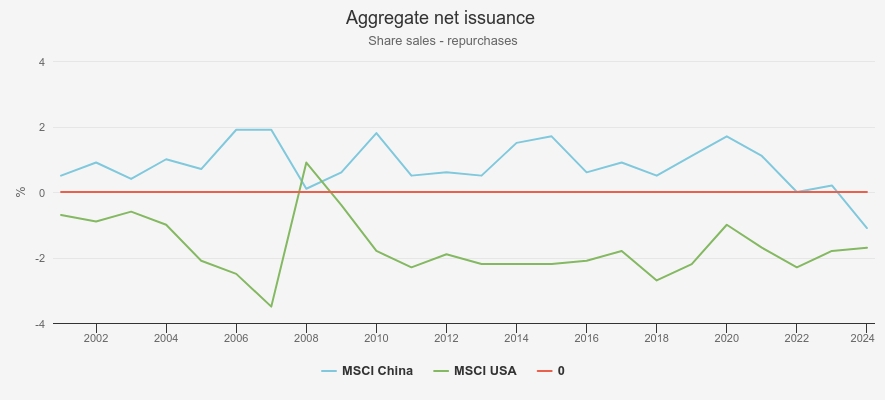

On aggregate, this has had a notable impact on the Chinese market. MSCI China’s net issuance turned negative for the first time this century in 2024, meaning there were more share repurchases than there were share issuances in the year. Not only has this been positive for share prices, but it also has a positive effect on future earnings per share as well. We think it is interesting to note how important buybacks have been to the US market’s dominant performance in recent years; if the Chinese authorities set out to encourage buybacks, it could be a powerful tailwind.

China’s net issuance

Source: Fidelity, as at 30/04/2025.

While the Chinese market has performed well in the period that these reforms have been rolled out, it is difficult to attribute how much influence they have had, as a result of all the other factors at play. In both Japan and Korea, it is possible to point to the reforms as a more obvious catalyst, although in China, the picture is more clouded, meaning the potential they still have to influence shareholder returns is difficult to predict

Further blurring the picture is the scepticism of the Chinese government. While the goal of the reforms is to adopt international practices to attract global investors, the government does have a history of poor treatment of minority, often international shareholders. Examples include the announcement that private education firms could no longer generate profit, wiping out an entire industry overnight and seeing many global investors see permanent loss of capital. Therefore, whilst these reforms look encouraging now, there is the potential for less helpful policy in future, and investors may remain sceptical after poor experiences in recent years.

However, we still think the focus on improving shareholder returns could be the catalyst for the next phase of the rally for China, as it was for Japan and Korea. Despite the turnaround in the past c. 18 months, returns from Chinese markets remain considerably behind both broader Asia and world indices over the longer term as a result of the challenges faced post-COVID. As a result, many investors argue the market remains attractively valued and therefore offers the potential for considerable upside.

Further adding to this is the notable discounts several trusts invested in the country continue to trade at. Every trust in the AIC China/Greater China sector is on a discount of around 9%, levels that are a couple of points wider than their five-year averages. Similarly, a number of trusts in the Asia Pacific and Asia Pacific Equity Income sectors with overweight allocations to China offer compelling discount opportunities, such as IAD on a discount of c. 9%, compared to a five-year average of 10.4%. Should the reforms in China be recognised, similar to how those in Japan and Korea did, we believe that not only could these trusts deliver strong NAV returns as their holdings reap the benefits, but returns to shareholders could be even stronger as discounts narrow as sentiment returns.

Conclusion

Just as Buddhism did not reshape Asia overnight, the corporate governance reforms that have reversed the journey across the continent have taken a decade to come to fruition. However, with Japan having become a proof of concept and Korea seeing results even quicker, having followed the blueprint, it now seems China is next to see the potential upside of executing corporate governance reforms.

While the fragmentary approach and clunky wording may have contributed to their potential for being overlooked, a number of investment trust managers have recognised this and have captured the benefits accordingly. Despite the better outlook for the country, not just as a result of the reforms but also an improving geopolitical situation, these trusts continue to trade at discounts in line with their five-year averages. As such, now could be the opportune moment for investors willing to follow the longer path to enlightenment.

Kepler Partners is a third-party supplier and not part of interactive investor. Neither Kepler Partners or interactive investor will be responsible for any losses that may be incurred as a result of a trading idea.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Important Information

Kepler Partners is not authorised to make recommendations to Retail Clients. This report is based on factual information only, and is solely for information purposes only and any views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment.

This report has been issued by Kepler Partners LLP solely for information purposes only and the views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment. If you are unclear about any of the information on this website or its suitability for you, please contact your financial or tax adviser, or an independent financial or tax adviser before making any investment or financial decisions.

The information provided on this website is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject Kepler Partners LLP to any registration requirement within such jurisdiction or country. Persons who access this information are required to inform themselves and to comply with any such restrictions. In particular, this website is exclusively for non-US Persons. The information in this website is not for distribution to and does not constitute an offer to sell or the solicitation of any offer to buy any securities in the United States of America to or for the benefit of US Persons.

This is a marketing document, should be considered non-independent research and is subject to the rules in COBS 12.3 relating to such research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research.

No representation or warranty, express or implied, is given by any person as to the accuracy or completeness of the information and no responsibility or liability is accepted for the accuracy or sufficiency of any of the information, for any errors, omissions or misstatements, negligent or otherwise. Any views and opinions, whilst given in good faith, are subject to change without notice.

This is not an official confirmation of terms and is not to be taken as advice to take any action in relation to any investment mentioned herein. Any prices or quotations contained herein are indicative only.

Kepler Partners LLP (including its partners, employees and representatives) or a connected person may have positions in or options on the securities detailed in this report, and may buy, sell or offer to purchase or sell such securities from time to time, but will at all times be subject to restrictions imposed by the firm's internal rules. A copy of the firm's conflict of interest policy is available on request.

Past performance is not necessarily a guide to the future. The value of investments can fall as well as rise and you may get back less than you invested when you decide to sell your investments. It is strongly recommended that Independent financial advice should be taken before entering into any financial transaction.

PLEASE SEE ALSO OUR TERMS AND CONDITIONS

Kepler Partners LLP is a limited liability partnership registered in England and Wales at 9/10 Savile Row, London W1S 3PF with registered number OC334771.

Kepler Partners LLP is authorised and regulated by the Financial Conduct Authority.